Is car insurance mandatory in Ontario?

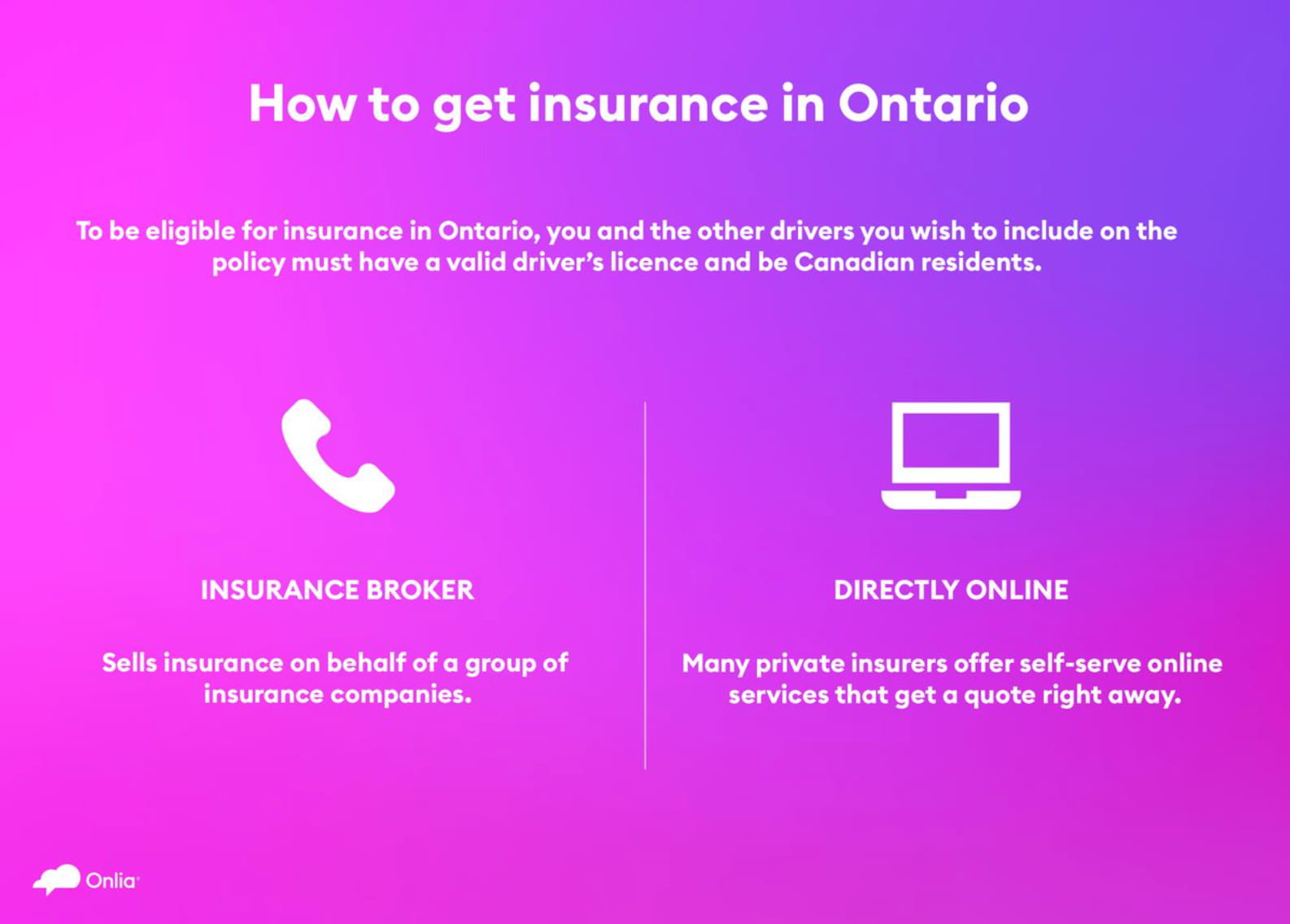

Yes. In this province, all registered vehicles must have insurance. Other provinces like BC and Manitoba have a government-owned insurer, but in Ontario you must purchase your coverage from a private insurer.

You’ll need to secure insurance coverage before you put licence plates on a car, renew your vehicle registration or buy a temporary permit, and the minimum fine for driving without insurance is $5,000. Repeat offences can cost up to $50,000, and you could have your driver’s licence suspended and your vehicle impounded.

Also, if you’re convicted of driving without insurance, you’ll likely have a hard time finding an insurance company that will insure you. Even if you do, you'll be charged higher premiums because you’ll be considered a high-risk driver.

How does car insurance work?

Before offering coverage options, most insurers will want to know things like the make and model of your car, the number of drivers in your household and how many kilometres your car travels in an average year.

Next, they’ll tell you what coverages are available. Car insurance is comprised of different levels of protection, limits and deductibles — you choose what's right for your needs.

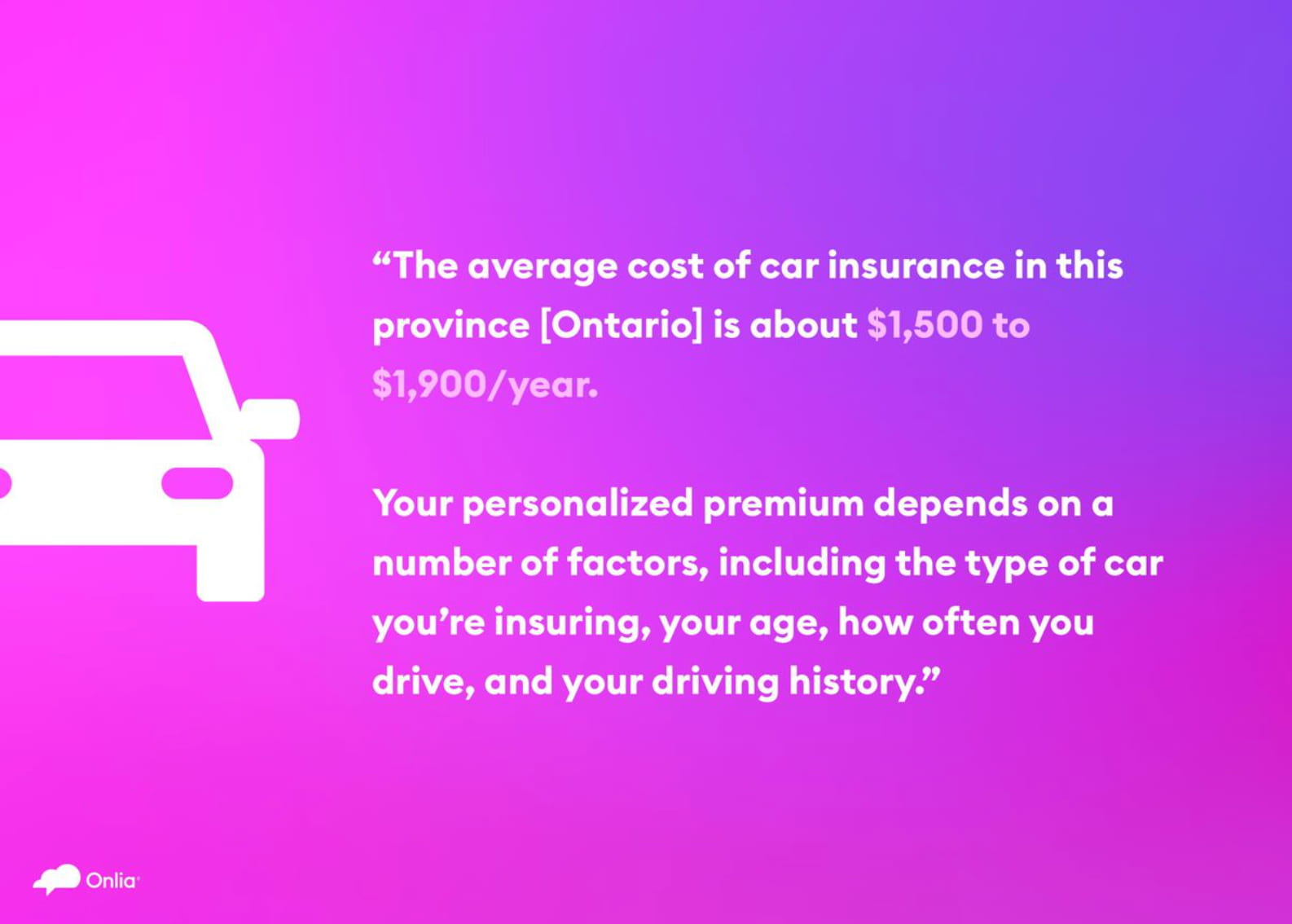

When you’ve settled on the protection you want, you’ll be given your premium: the amount that you pay for your coverage. Many people pay monthly premiums, but most insurance carriers allow you to pay quarterly or annually, both of which can save you money.

Which insurance coverages are mandatory?

As a car owner and driver, you are required to purchase these coverages:

- Accident benefits. Covers the cost of medical expenses and any ongoing treatments you might need as you recover from an injury caused by a collision involving your car. It will also provide income replacement if you’re unable to work while you recover.

- Third-party liability. Covers the costs when someone outside your vehicle is injured or killed, or property is damaged because of an accident involving your car, up to $200,000. Note: Liability claims often run into the millions of dollars, especially if someone is hurt in a collision. Most Ontario drivers opt to upgrade third-party liability coverage to cover $1 million or more.

- Uninsured automobile. Provides up to $200,000 for damages if you’re injured or killed in an accident that involves an uninsured vehicle or a driver that leaves the scene.

What other coverages can I get?

In addition to the mandatory coverages, you have other optional protections available.

You can raise the limits for the third-party liability coverage and accident benefits coverages to be more in line with what damages would cost today.

Optional accident benefits

These are optional coverages that provide protection in specific situations:

- Income replacement benefits

- Medical, rehabilitation and attendant care benefits

- Caregiver benefits

- Housekeeping and home maintenance benefits

- Death and funeral benefits

Each coverage comes with its own coverage limits. It may be helpful to talk to your insurer about which ones may be worthwhile for you.

Extra coverage for loss and damage to your vehicle

Do you love your car? Many people choose to add coverages like these to fully protect their car from all types of unexpected accidents:

- Specified perils coverage. This pays for losses caused by things like fire, hail, floods or theft.

- Collision or upset coverage. This one is very popular! It pays for damages if your vehicle is in a collision with another object or rolls over.

- Comprehensive coverage. This is protection for losses that come from perils other than collision or upset.

- Direct Compensation — Property Damage (DCPD). This pays to repair damage to your vehicle and any belongings in it after an accident that isn’t your fault.

- All perils coverage. This is a combination of collision or upset and comprehensive coverages. It also covers loss or damage if a member of your household steals your car and provides protection if an employee uses it.

Optional policy endorsements

An endorsement is an extra benefit you can add to your insurance policy to change, add or reduce the amount of coverage in certain situations such as:

- Rented or leased vehicles

- Transportation replacement when your car is being repaired

- Liability for damage to non-owned automobiles

- Family protection coverage

Your insurance provider will offer details that will help you decide what makes the most sense for you.